By Emily Martin

Shymee Davis sat at her desk and pointed to a tan and blue box, full of Post Great Grains Blueberry Morning cereal. She said she had taught seniors the health benefits of cranberries and antioxidants just moments ago.

“I try to introduce them to things they ordinarily don’t eat,” Davis said in an interview. “I try to broaden their horizons, so every week I come with something different, and with that, I like to give them the benefits or nutrients that are involved.”

Shymee Davis is a nutritionist at the Washington Seniors Wellness Center in Ward 7, and she teaches nutrition education classes as part of the nutrition program. Davis said a senior brought her the opened box of cereal and asked if the cereal had antioxidants; it did not.

Many seniors and retirees living in Washington, D.C. rely on nutrition programs, like the Weekend Nutrition Program at the senior center where Davis works, to get information about nutrition or for their next meal. Many more are not as lucky and need to apply for monthly benefits from the Supplemental Nutrition Assistance Program (SNAP) because their only source of income may be a family member’s or from Social Security checks.

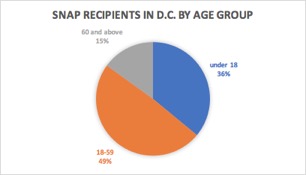

D.C. Department of Human Services, which runs the SNAP program, found that out of approximately 100,000 individuals on the program, 15 percent are over the age of 60, which is the smallest age group compared to nearly half being between 18 and 59. However, the Food Research and Action Center, a non-profit research organization focused on food insecurity, estimated the number at 16.3 percent, placing D.C. in the top ten metro areas with the most seniors participating in SNAP and six percent over the national average.

According to Melissa Jensen, an anti-hunger program associate who specializes in SNAP at advocacy group D.C. Hunger Solutions, the government benefits program has become a part of retirement for many D.C. residents, especially in Wards 7 and 8.

“It’s a growing problem across the country, largely because seniors plan to retire on their social security, especially seniors who worked low-income jobs or hourly jobs, which, when you’re in the workforce, doesn’t let them build a lot of savings,” Jensen said in an interview.

Jensen said retirees live off of Social Security, which will not cover all their expenses, and they move in with family members or rely on SNAP to make ends meet. She also said that many seniors find it too difficult to apply for SNAP because there is no online application, and waiting at a service center to be interviewed and approved can take hours. On top of that, if a senior is on a fixed income like Social Security, they will only qualify for the minimum benefit of $30.

“It’s so much work for only $30 a month,” Jensen said. “A lot of the times, if they don’t have a resource like [me] or they don’t know how to contact us or someone else to advocate for them, it just seems like a very mysterious process.”

The minimum for SNAP benefits can actually be as low as $16. Brian Campbell, a senior policy advisor at the Economic Security Administration, a branch of DHS, said in an interview that the rest of the $30 minimum that Jensen mentioned comes from locally-funded benefits. Campbell said the D.C. Council passed law 4–261, effective in 2015, which required local benefits be allocated to households that received federal benefits below $30 a month, bringing their total up to $30.

Campbell said simplification of the application is already in the works. He predicted that residents can expect an online customer portal for the SNAP program to debut within the next 24 to 36 months. The release is currently undergoing requirement testing.

“The trick is, how much time do we spend, how many resources do we spend on program integrity,” Campbell said in an interview. “There’s always going to be some element of imperfection, but we need to strike a reasonable balance in terms of doing our due diligence.”

Campbell said part of that due diligence is the required interview, but this release will soon allow for phone interviews, making the process more accessible to seniors with mobility or medical issues who cannot travel to service centers.

Jensen, however, said that on top of these challenges, some seniors still find themselves ineligible. The DHS website caps gross maximum income for eligible households with one member at nearly $2,000, but adding additional members increases the maximum income by $694 per member.

Alison Jacknowitz, a senior associate dean in American University’s Department of Public Administration and Policy, is an expert in the field of food insecurity, specifically involving children. She said most of the government-based food assistance programs are targeted towards children and their families, which can discourage seniors from applying, even if they are eligible.

“The criteria to get on the program, and transactional costs of getting to offices or going food shopping or cooking, makes some of these programs less enticing to seniors,” Jacknowitz said in an interview. “We [see] that seniors [are] less likely to use the program among those who are eligible, and it could be because it’s harder for them to maneuver through the system.”

For seniors who do not meet the requirements or do not apply, Jensen said they can go to senior wellness centers or food banks to get necessary food, yet there are still challenges.

Campbell said that these alternatives may not work for some because of their specific needs, and traveling to a center or food bank may be difficult if a meal delivery service does not cater to their area.

“Depending on where a senior lives, you might have resources to food, but is there access to food? So with the proximity which one lives to markets, and being on a transit route, that’s certainly an issue, especially in Wards 7 and 8 and parts of Ward 5,” Campbell said. “There simply aren’t a lot of shopping options … and it’s harder for seniors to get around, so how do they get access to specifically healthier foods?”

Jensen added that access to healthy food is limited, and the nutrition seniors find with these resources might not meet their dietary restrictions. Jensen referred to her organization’s 2016 report of a food desert in Wards 7 and 8, where there are only three grocery stores that supply processed foods to residents in the area, causing issues for seniors with dietary needs.

The Washington Senior Wellness Center works to rectify this by providing daily healthy meals and weekly nutrition education classes for seniors in Ward 7, according to Davis.

Davis also said that representatives of the Senior Farmers’ Market Nutrition Program, a Department of Agriculture program that provides low-income seniors with coupons for farmers’ markets, often visit the center to encourage buying fresh produce. These programs help seniors obtain meals, Davis said, but there are other benefits to attending a wellness center.

“Here, they’re more mobile, and happier because they’re active, engaged and involved in the activities,” Davis said. “I would encourage seniors immediately when you retire, to come to the wellness center because it helps you to remain healthy.”

Jacknowitz said the solution to food insecurity may be more long-term like Davis suggested.

“There’s two tracks. I think there’s a track that will deal more with structural issues under unemployment and poverty, and so that might be training or education,” Jacknowitz said. “But then there’s also the track of how do we help people in the immediate term because they need food immediately.”

Jacknowitz said that community-based programs are becoming more common as government-run programs, like SNAP, experience budget cuts or eligibility changes, yet they will not replace them.

While Jensen said these senior populations are still underserved in D.C. when it comes to nutrition, there is also an issue of financially planning for retirement without having to rely on Social Security. The social insurance program is meant to supplement a retiree’s source of income or savings, not replace it, but many people cannot afford to save money because they worked low-income or part-time jobs.

Joshua Dorfman, a financial advisor at a D.C. branch of Northwestern Mutual, said that saving for retirement is not as common because many people are not taught to save early on in their careers.

“Starting in your 20s and 30s puts you head and shoulders above folks that start in their 40s and 50s, but unfortunately, not everyone is aware of that,” Dorfman said in an interview. “It might just be that it’s an intimidating discussion, they don’t know who to turn to for advice … or it could simply be that, based upon their income, they don’t feel they’re in a position to save.”

Dorfman said he believes the epidemic of insufficient retirement savings could be solved through promoting financial literacy at home and in schools.

“Someone’s openness to a discussion often times has very little to do with how much they make,” Dorfman said. “A lot of folks view talking about money as taboo, and I think promoting a society where people feel comfortable having that discussion, regardless of what their standing is, that would make an impact.”

Retirement for low-income households can be difficult, especially in a city where the cost of living has soared in recent years. Business Insider found in August that the average rent for a two-bedroom apartment is nearly $3,000 a month, while the Census Bureau’s 2016 American Community Survey found that the per capita income in Ward 8 is $18,787, only two-fifths the D.C. per capita income.

Dorfman said it is difficult to live on Social Security in D.C. after making non-discretionary purchases like healthcare and rent. Furthermore, Dorfman said a majority of people retire unexpectedly due to health problems, which can lead to retirees relying on family members for healthcare or using most of their Social Security to cover it, leaving little money for other expenses like food.

Retiring in D.C., a city with a high standard of living, after working a low-income job your whole life can prove to be an arduous task, as Jensen, Dorfman and Campbell put it. Relying on Social Security can make it even more difficult, since a 2016 annual report from the Social Security Administration’s Board of Trustees estimated that the trust fund reserves may become depleted by 2023, leaving workers questioning how they will be able to retire.

“The question is if we’ll become more reliant on programs like SNAP or we’ll just have to find other means of funding retirement,” Jensen said. “I think it’s a sign of the importance of funding these programs and continuing to fund them for the future because as other programs wane, things like SNAP are key to so many people getting proper nutrition.”

Audio: https://soundcloud.com/emily-martin-934391204/ar-final-project-audio

concerned him because “obviously the status quo isn’t working” and he believes the governor, senators, congressmen and public officials elected in Florida’s midterm elections need to do “something.”

concerned him because “obviously the status quo isn’t working” and he believes the governor, senators, congressmen and public officials elected in Florida’s midterm elections need to do “something.” aspects of her life, including politics. She believes the most important issue facing the world is climate change and that it is overlooked at our own risk.

aspects of her life, including politics. She believes the most important issue facing the world is climate change and that it is overlooked at our own risk.